Medical debt 🤕

My homework this month for my advocacy training program is all about medical debt. It’s not a fun topic, for sure, but it’s an important one.

We began by reading a couple of research articles that shared statistics and trends about health care costs and medical debt. Here are some of the key points from one of those articles [excerpts selected by me]:

Just under half of U.S. adults say it is difficult to afford health care costs. One in four say they or a family member in their household had problems paying for health care in the past 12 months.

The cost of health care can lead some to put off needed care. About one-third (36%) of adults say that in the past 12 months they have skipped or postponed getting health care they needed because of the cost.

The cost of prescription drugs prevents some people from filling prescriptions. About one in five adults (21%) say they have not filled a prescription because of the cost while a similar share (23%) say they have instead opted for over-the-counter alternatives. About one in seven adults say they have cut pills in half or skipped doses of medicine in the last year because of the cost.

Health care debt is a burden for a large share of Americans. In 2022, about four in ten adults (41%) reported having debt due to medical or dental bills including debts owed to credit cards, collections agencies, family and friends, banks, and other lenders.

Those who are covered by health insurance are not immune to the burden of health care costs. Almost four in ten insured adults under the age of 65 (38%) worry about affording their monthly health insurance premium and large shares of adults with employer-sponsored insurance (ESI) and those with Marketplace coverage rate their insurance as “fair” or “poor” when it comes to their monthly premium and to out-of-pocket costs to see a doctor.

Does any of this sound familiar? I immediately felt seen, and I anticipate many of you will feel the same. Of these, from my life largely within the world of higher education and nonprofits, I’m used to conversations about the high cost of health insurance, and about how it seems like we are paying more but getting less. But conversations regarding debt and fear of debt a little less easy and carry a bit more shame.

Here’s some of what I shared with my cohort earlier this week and some of what I’ve been thinking about since then:

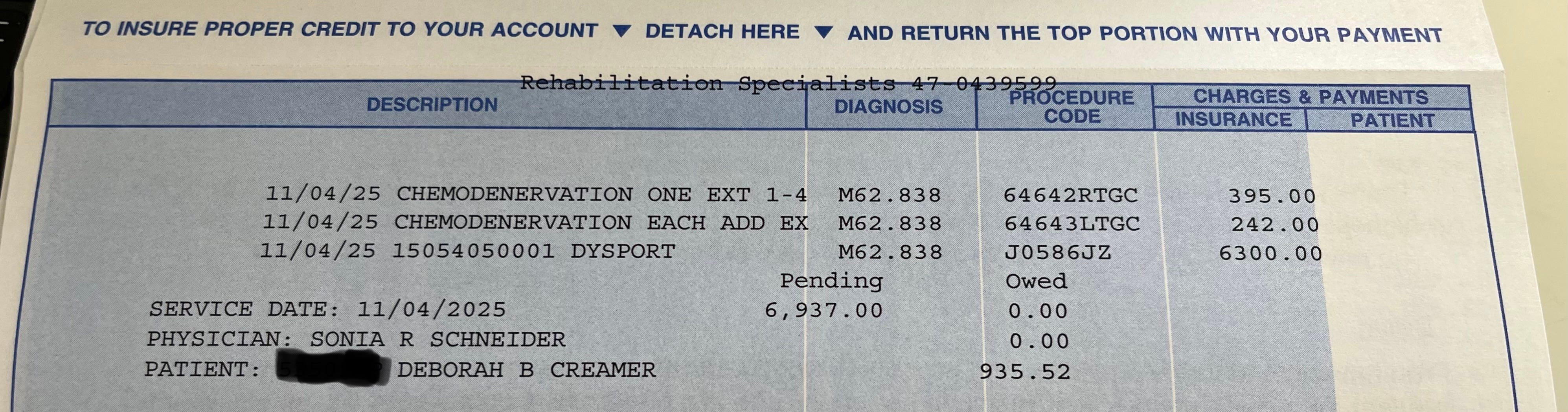

My bill for the first month of care following my spinal cord injury (including surgeries and time in the ICU) was $800,000.

I was fortunate to have very good private insurance. It still took at least half a dozen informal inquiries, two formal appeal processes, and more than a year to get some of those charges corrected (I’m sure the hospital didn’t intend to bill me twice for a number of expenses!) and to get the rest of those charges covered (among other things, my insurance refused to pay for one of the surgeries because prior authorization hadn’t been requested…so I had to convince them the alternative was my death ☠️).

Throughout time in rehab, decisions about my care were frequently made by the insurance company, not my own medical professionals.

Key among these was the decision as to whether I could even stay in rehab or not. After my initial weeks in each program, the insurance company would approve my continuation just one week at a time, and sometimes made that decision just a single day in advance. I remember an especially terrifying time when my facility’s doctor was waiting for the insurance switchboard to open one morning just to plead my case; otherwise they would’ve had to release me that afternoon. I had nowhere to go, and no way to get there, and everyone involved thought their hands were tied. No, it was just me who was a prisoner to a system that was not designed with my health in mind.

When I got to long-term care (a.k.a. the nursing home), none of my care beyond medications and doctor visits was covered by insurance. This meant I had to write my facility a check for more than $13,000 every month.

And no, that’s not excessive for a nursing home, especially since I was committed to having a private room. We did find a few cheaper ones in the Omaha area, but only with poor inspection ratings. We also found more expensive ones, and ones with a similar base cost but also more supplemental costs. I imagine the overall cost would be higher in other parts of the country/world (and lower in other parts as well). Here’s a calculator if you’re curious. FYI, most insurance does not cover nursing home care, as they classify it as a convenience. If you think you might be headed in that direction, and you’re not already qualified for Medicaid, you might want to look into long-term care insurance or other plans.

Now that I’m at home, my caregiver costs have actually gone up. I pay about $3000 a week for care, and this (unlike the nursing home) does not include rent, food, or any of the other expenses of daily living. My quality of life (including my health) has gotten so much better, so it is definitely worth it, even if it means thinking of this as my retirement.

Once my employer stopped funding my health insurance premiums, I elected to continue it through COBRA until I became eligible for Medicare (two years after Social Security I had the determination that I was permanently disabled). This meant sending in a check for more than $1000 a month, on top of my deductible, co-pays, prescriptions, and non-covered expenses.

I did look at alternatives on the Marketplace, and even with the affordable care act subsidies still in place, I couldn’t find a better option in terms of coverage and cost. As of December 2025, I am now on Medicare and things have become affordable again. This convinces me more than ever that insurance is an utterly broken system.

That said, just within just the last two weeks (now that I have switched to Medicare), we have made a number of decisions about my prescriptions solely on cost.

In one case, the dose my doctor requested (6 mg) was not covered but a different dose (2 mg) was covered, so she adjusted the prescription to be three pills rather than one, saving me about $600 a month. In another case, a different doctor gave me a prescription for a less effective medication when the one she first requested came back as not covered by any Medicare plan I’m eligible for. We will try this alternative and monitor it, and then see what other steps we might need to take.

I have been sent to collections at least three times (so far) for unpaid bills.

Once was my fault (I simply missed a bill) and the other two times were billing and/or insurance issues. It amazes me how quickly this happens, and how ordinary it is. I also get bills that aren’t accurate (including some fraud and some ordinary human errors), and some of the billing happens so slowly. And I play a juggling game of figuring out where to move my money at the right time in order to cover what needs to be covered.

Exhausted? So am I – and this whole business level is so far removed from staying well and getting stronger and living my best life. I have been so very fortunate that I saved so much of what I earned when I was working ATS (and that I was paid so well for that work) so I have reserves to pay for all these expenses, for a while yet. And I’m also so very fortunate to have skills and abilities that allow me to navigate these systems as well as do – I’m organized, assertive, well spoken, persuasive, “nice” older/younger white lady, and so on. And I’ve had time and enough energy to stay on top of much of this. It pains me to think of people who are trying to navigate all of this with fewer resources than I have.

But let me return to the research excerpts that I started with. These stories are not unique to someone like me. We are all dealing with this. I don’t know that talking about it more amongst ourselves helps, but it does help me let go of some of the stigma and shame. And I hope from that energy I can bring some of this forward to those who are not dealing with these levels of stress and burden – as I was recently reminded, my state’s legislators are largely wealthy and/or retired people who may remember systems that are or were less broken in their experience experiences. And this again is where I’m excited about my advocacy training program, hoping I can learn to use my stories and my voice to make a difference.

Brilliant. I’m assuming that I can pass this on outside Substack?

I mean, I’m not assuming so hard that I’m doing it without permission.

So much so. Thank you, Debbie, for putting this out there. My spouse and I have carried medical debt for years since her multiple surgeries despite Medicare and other insurance. Just today I asked one of her doctors to rewrite a script because the specific dosage wasn’t in her insurance’s formulary for her. Hours of my time…. And we had well paying jobs with insurance before all of this. Thanks again for your advocacy via Substack, Debbie.